RESPs (Education Funds)

Early this year our family grew and we became lucky new parents with our wonderful baby girl. When my wife and I went to the hospital, I signed up at the hospital to get contacted by someone who was an expert in RESP's, (which stands for Registered Education Savings Plan.).

Now, what was told to me about this program was basically this:

I, the parent, pay into it, and the government will also help pay a little bit into it.

By 18 or by the time your child goes to post-secondary. The child will need to do 13-weeks of school to get access to the money.

When they (the child) are given the money for school, they get charged income tax on it.

The real win here is that the growth of the RESP is tax free, and the government contributes a portion of money.

There is a $50,000 life-time maximum (per child) on the RESP.

The Bank (this coming from the representative I spoke to) can handle the RESP account for us. They'll get us something like 3% return every year (not a hard promise, but a probable return).

They (the Bank) take fee's to manage the RESP for you (somewhere along the lines of 25%)

Now, this sounds pretty decent, I make some contributions, and make some tax-free growth, but is it really that good? Let’s break this down a bit more, because as I've discovered... the devil is in the details!

So what I first noticed is if you want to get the full amount of government money you need to contribute about $2500 per year. Now, putting in this $2500 per year can get you anywhere from $500 to $600 per year depending on your income bracket.

So, lets do some quick math:

$50,000 (the max that is allowed to be contributed to the RESP) divided by 2500 = 20 years. Which means it takes me 20 year to contribute the per-child RESP maximum before I’m not allowed to contribute anymore. Now, with the government assistance, the max is hit even sooner. Looking at the math it becomes:

50,000 / (2500 + 500) = 50,000/3000 = 16.6 years. However there is a max the government will contribute from the CESG program of $7,200, and when we calculate how long it takes for the government to give out its CESG amount it takes about 14.4 years. Looking at the math: ($7,200 CESG / $500 per year = 14.4 years)

Now, the following was basically what was being promoted by the bank representative:

We (the parents) pay $2500 per year (about $208.33 per month) and get the $500 per year from the Government, and put it into an RESP account with the bank.

The bank will manage this RESP portfolio, getting us maaaaaybe 3% (based on their past performance), but we pay a hefty RESP management fee.

Let’s call this Scenario “A”, but let’s not include the management fee, so we can compare apples-to-apples.

Next, let's look at another way of approaching the RESP. The life-time maximum is 50,000. What happens if we put 49,500 into the RESP account right away? Well, for one we don't get the government match. Actually, I think we only get it once ($500) since in the first year we will have exceeded the $2500 needed to get the yearly government match. So, given we put in $49,500 and get $500 from the Government, we would have $50,000 in the RESP in year 1, and let’s say (to keep it the same comparison) it also grows at 3% Year-over-Year. Let’s call this Scenario “B”.

Now, what's super neat about Scenario B, is that the money grows tax-free for the full 18 years (since we deposited up front in year 1). So let's check these Scenario’s out in WealthNav!

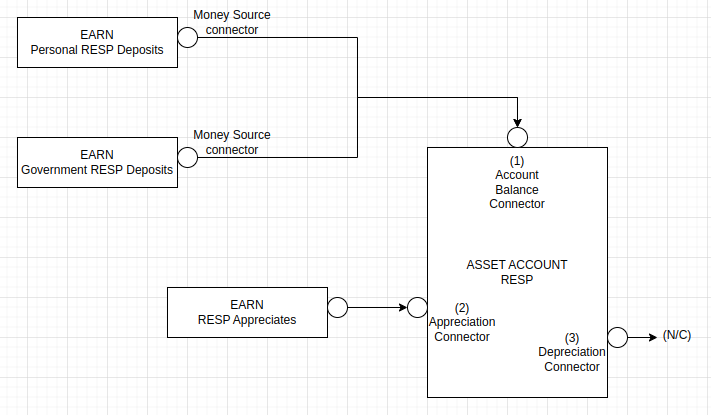

In WealthNav I would have setup 2 Earn accounts and action (lines). 1 account-and-action will be the personal $2500 per year contribution, the other, the government match of 500/year. Also, you will see a third Earn account (which provides the Appreciation amount. If this is confusing, try going through my in-depth tutorial of a financial setup here) I also setup an Asset (unrealized) account called "RESP" and set its Year-over-Year to 3%. Let’s see what the financial picture of this would look like:

Diagram 1: Financial Picture of RESP with Contributions

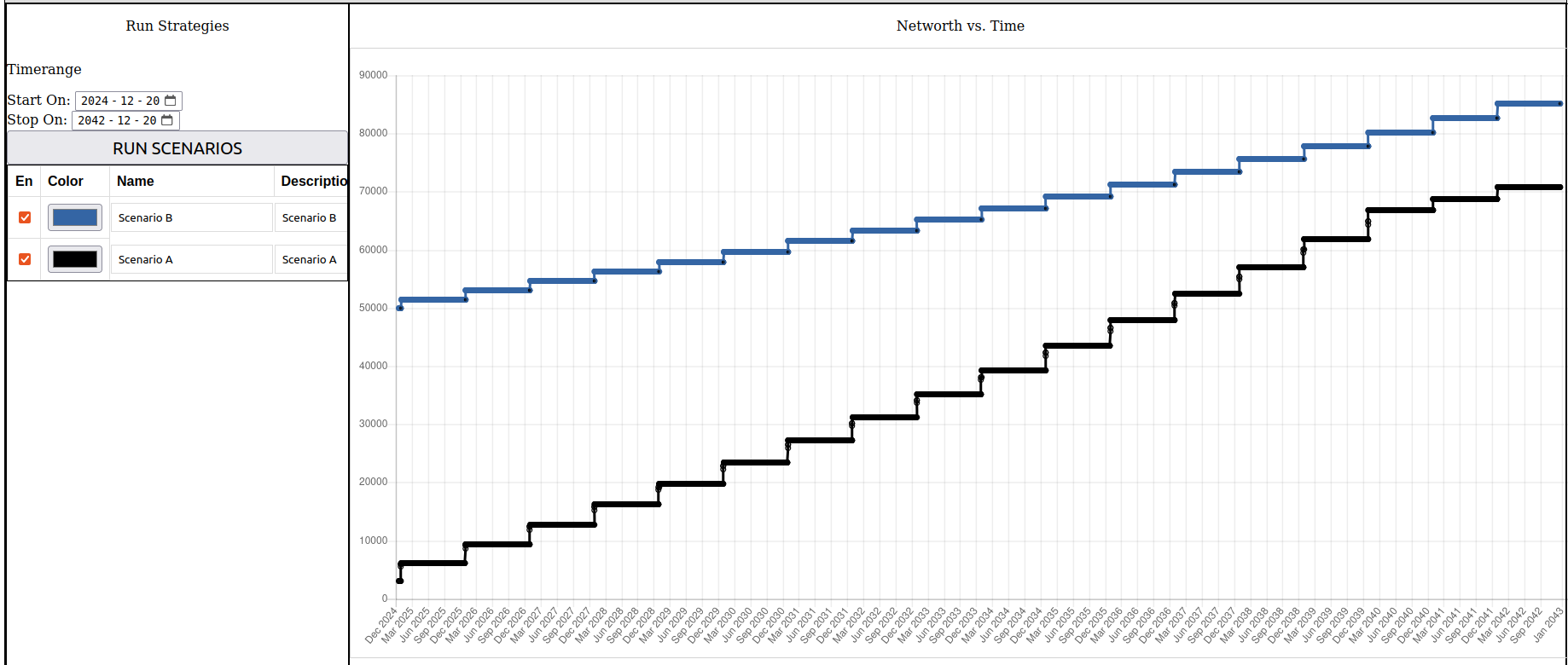

For the second scenario (which is blue in the following net-worth graph). I have the exact same financial picture setup, but instead of adding $2,500 per year, I do a 1-off contribution of $49,500, and 1-off contribution from the government for $500.

Diagram 2: RESP value after 18 Years for 2 Scenario’s at 3% Growth Year-Over-Year

In the diagram the net-worth of the Blue (Scenario “B”) is at $85,121.65. The net-worth of the Black (Scenario “A”) is at $70,864.43. So just by loading the RESP up front and missing out on the Government matching we make an extra: $14,257.22

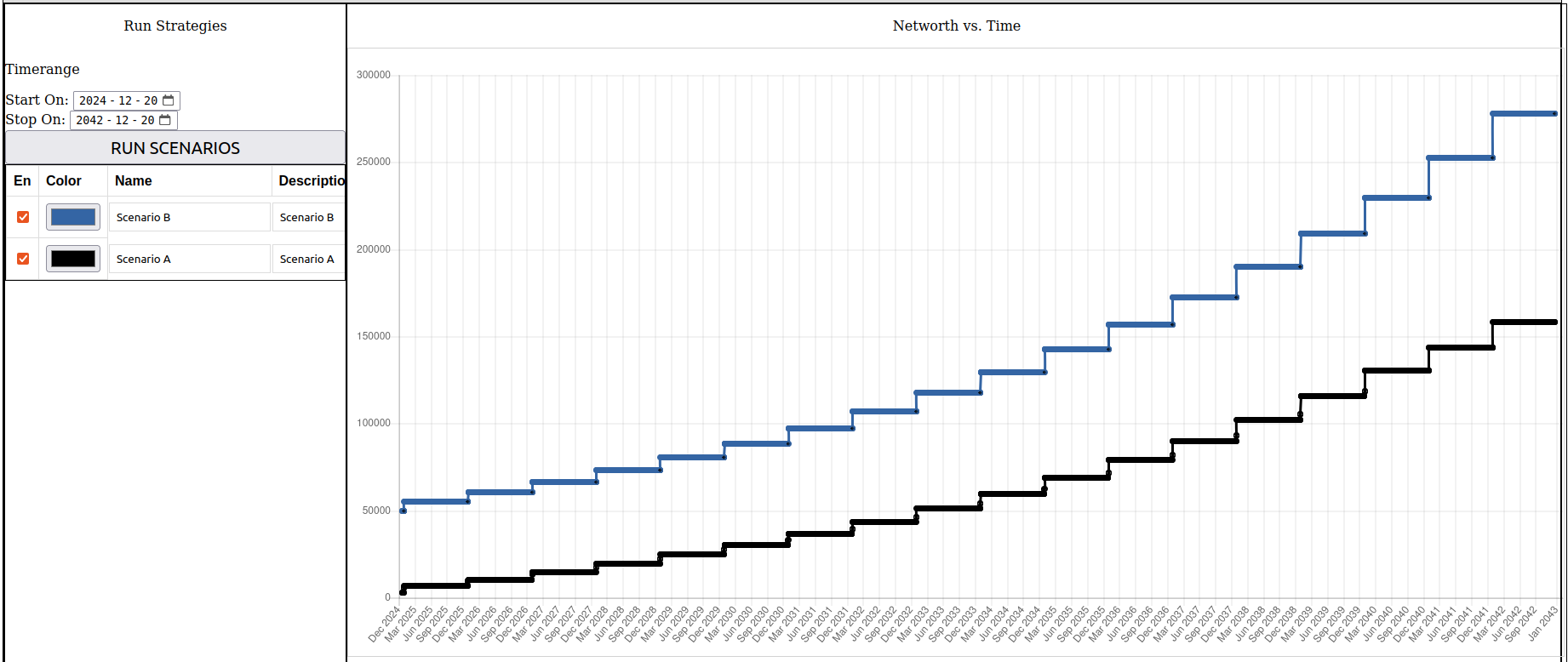

Now, I had mentioned that we would keep the growth rates the same, and I picked 3% because the bank reps told me they could likely achieve this. But, if I look at VanGuard’s S&P 500 (ticker symbol: VOO) ETF, I can see their 10-year average is something along the lines of: 13.3% per year (and the Category benchmark is around 11.9%. See performance here). So, let’s see how this would play out if we had used a slightly more conservative 10% return, and to keep apples-to-apples, I will assume 10% for both scenario’s:

Diagram 3: RESP value after 18 Years for 2 Scenario’s at 10% Growth Year-Over-Year

In diagram 3 above, now we see that the blue line (Scenario “B”) grew to $277,995.86, and the black line (Scenario “A”) grew to $158,052.96, and now the difference between methods is around: $119,942.90. This is the power of tax-free growth of lump sums up front!

Now, I didn’t cover the cost of using the Bank’s representatives, but generally their fee’s destroy the early gains I could see in my stocks, so coupled with a 3% “probable” return they said I could get, it makes more sense for me to just manage the RESP myself with someone like Questrade, stick it in an ETF that has a decent long-term average and let it grow on its own. This is not financial advice, just something that I’m looking at doing myself.